1. What is this new update?

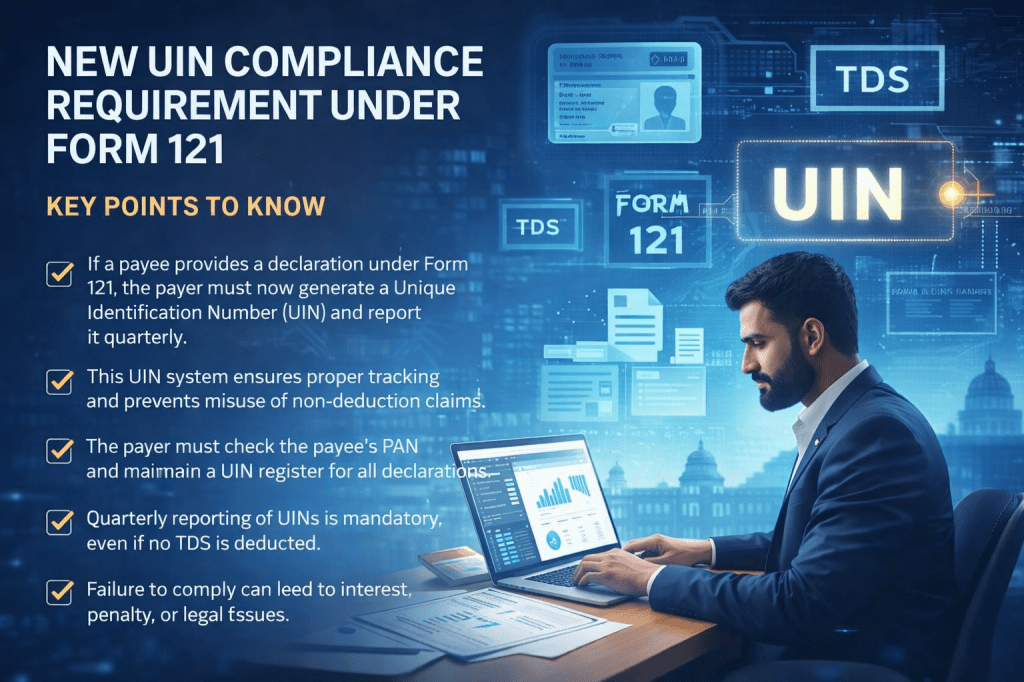

CBDT has introduced a new compliance requirement through its Notification dated 28.03.2026 for declarations filed in Form 121. Now, wherever a payee gives a declaration for non-deduction of TDS, the payer has to generate a Unique Identification Number (UIN) for that declaration and report it in the prescribed manner. In simple terms, the government now wants every such declaration to be properly tracked and linked in the system.

2. Why has UIN been introduced?

The main purpose of UIN is to bring transparency, traceability and control in TDS compliance. Earlier, declarations were mostly kept as internal records by the payer. Now, the department wants each declaration to be uniquely identified so that it can verify whether non-deduction of tax was actually backed by a valid declaration. This reduces chances of duplication, misuse, incorrect claims and future disputes.

3. What does the payer have to do?

The payer has to:

- receive the declaration in Part A of Form 121

- verify the details, especially PAN

- generate a 26-character UIN

- maintain proper records

- file Part B of Form 121 quarterly on the income-tax portal

A very important point is that this reporting obligation continues even if no tax was actually deducted during the quarter. So this is not just a document collection exercise; it is now a proper reporting compliance.

4. What are the practical risks if this is ignored?

If the declaration is defective, PAN is wrong, UIN is not generated, or quarterly reporting is missed, the payer may face compliance issues. In such cases, the department may question the non-deduction of tax and the payer may be exposed to interest, penalty or TDS default consequences. Therefore, businesses should not treat Form 121 as a casual paper form anymore. It now carries system-based compliance importance.

5. What should businesses and professionals do now?

Businesses, accountants and CAs should immediately put a proper process in place for:

- collecting declarations on time

- checking PAN and other details

- allotting UIN properly

- maintaining a declaration/UIN register

- reconciling quarterly reporting with TDS records

The overall message is simple: if tax is not deducted based on Form 121, that declaration must now be digitally traceable through UIN. This is a compliance-focused reform, and timely system setup will help avoid future notices and disputes.

Leave a comment