The Draft Income-tax Rules, 2026 propose a significant restructuring and renumbering of several compliance forms. The objective is to consolidate, standardise, and modernise the compliance framework.

Unlike ITR forms (ITR-1 to ITR-7), these changes affect audit reports, TDS statements, registration forms, and reporting formats.

This article explains the major proposed renumbering.

Why Is Renumbering Being Done?

The Draft IT Rules 2026 aim to:

- Consolidate scattered rule-based forms

- Introduce logical numerical sequencing

- Reduce duplication

- Align digital compliance formats

- Modernise tax administration structure

This is a structural reform, not just cosmetic renaming.

Major Form Changes Explained Individually

1. Tax Audit Report

Old Forms: 3CA / 3CB / 3CD

Proposed New Form: Form 26

The separate audit report formats are proposed to be consolidated into a unified new numbering system.

2. Transfer Pricing Report

Old Form: 3CEB

Proposed New Form: Form 48

Transfer pricing certification form is proposed to be renumbered under the new structure.

3. MAT Certificate

Old Form: 29B

Proposed New Form: Form 66

The MAT certification form is proposed to shift into the revised numbering framework.

4. Charitable Registration

Old Form: 10A

Proposed New Form: Form 104

Registration application for charitable trusts is proposed to be renumbered.

5. NGO Audit Report

Old Forms: 10B / 10BB

Proposed New Form: Form 138

Audit reporting for charitable institutions is proposed to be consolidated.

6. Salary TDS Return

Old Form: 24Q

Proposed New Form: Form 132

Quarterly TDS return for salary payments is proposed to receive a new number.

7. TDS Return (Non-Salary)

Old Form: 26Q

Proposed New Form: Form 143

Non-salary TDS statement is proposed to be renumbered.

8. TCS Return

Old Form: 27EQ

Proposed New Form: Form 143 (as per draft summary reference)

This indicates consolidation under the new numbering series.

9. Foreign Remittance Reporting

Old Form: 15CA

Proposed New Form: Form 145

Reporting for foreign remittances is proposed to shift under new numbering.

10. Annual Information Statement

Old Form: 26AS

Proposed New Form: Form 168

Form 26AS is proposed to be replaced or renumbered under the revised format structure.

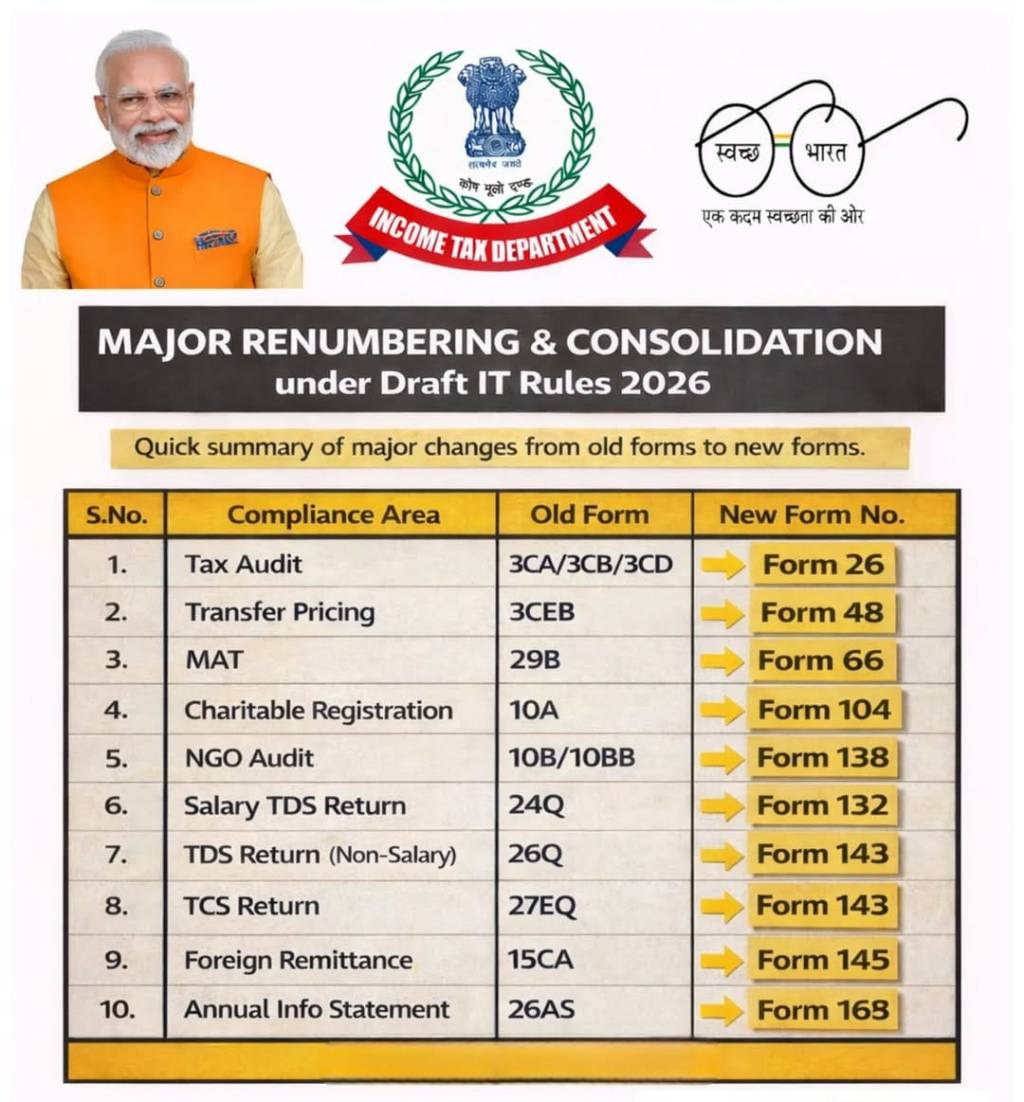

Old vs New Form Numbers – Comparison Table

| S.No | Compliance Area | Old Form | Proposed New Form |

|---|---|---|---|

| 1 | Tax Audit | 3CA / 3CB / 3CD | Form 26 |

| 2 | Transfer Pricing | 3CEB | Form 48 |

| 3 | MAT Certificate | 29B | Form 66 |

| 4 | Charitable Registration | 10A | Form 104 |

| 5 | NGO Audit | 10B / 10BB | Form 138 |

| 6 | Salary TDS Return | 24Q | Form 132 |

| 7 | TDS Return (Non-Salary) | 26Q | Form 143 |

| 8 | TCS Return | 27EQ | Form 143 |

| 9 | Foreign Remittance | 15CA | Form 145 |

| 10 | Annual Information Statement | 26AS | Form 168 |

Important Clarification

These changes are based on Draft IT Rules 2026 and are subject to final notification. Until officially notified, existing form numbers continue to apply.

Professionals should:

- Monitor CBDT notifications

- Avoid premature migration

- Verify portal updates before implementation

Conclusion

The Draft IT Rules 2026 indicate one of the biggest structural reorganizations of income tax compliance forms in recent years. While ITR forms (ITR-1 to ITR-7) remain unchanged, several audit, TDS, and reporting forms are proposed to be renumbered and consolidated.

Tax professionals must stay updated to ensure smooth transition once final rules are notified.

FAQs

1. Are these new form numbers already applicable?

No. The changes are part of the Draft IT Rules 2026 and will apply only after final notification by the government.

2. Are ITR-1 to ITR-7 being renamed?

No. The renumbering proposal mainly affects statutory compliance forms like audit reports, TDS returns, and reporting forms — not the main ITR return forms.

3. Is Form 24Q being replaced by Form 132 immediately?

Not yet. Until official notification and portal update, Form 24Q continues to remain valid.

4. Why is the government renumbering these forms?

The objective is consolidation, logical sequencing, reduction of duplication, and alignment with a digital compliance framework.

5. Will existing filing utilities change?

Yes, once notified, the Income Tax e-filing portal and utilities are expected to update the new form numbers accordingly.

6. Should professionals start using the new numbers now?

No. Continue using existing form numbers until CBDT officially implements the revised rules.

7. Does this affect tax audit reporting formats?

Yes. Forms like 3CA/3CB/3CD are proposed to be consolidated and renumbered under the new draft framework.

8. What happens to Form 26AS?

Under the draft proposal, it is suggested to be renumbered as Form 168, subject to final notification.

Leave a comment